- Products

Saakuru Blockchain

Blockchain with no gas fee

Learn more

Saakuru App

All-In-One crypto wallet

Learn more

Saakuru SDK

Embed Web3 wallet easily

More Info

dApp Store

Discover Thousands of dApps

Learn more

Saakuru Games

Guild Management Tool

Apply for scholarship

TomoOne

Grow virtual pet

Learn more

Saakuru Cashback

Shop online with discount

Learn more

Saakuru Blockchain

Blockchain with no gas fee

Learn more

Saakuru App

All-In-One crypto wallet

Learn more

Saakuru SDK

Embed Web3 wallet easily

More Info

dApp Store

Discover Thousands of dApps

Learn more

Saakuru Games

Guild Management Tool

Apply for scholarship

TomoOne

Grow virtual pet

Learn more

Saakuru Cashback

Shop online with discount

Learn more

- Token

- Academy

- Saakuru Live

- About us

- Community

Products

Saakuru Blockchain

Blockchain with no gas fee

Saakuru App

All-In-One crypto wallet

Saakuru SDK

Embed Web3 wallet easily

dApp Store

Discover Thousands of dApps

Saakuru Games

Guild Management Tool

TomoOne

Grow virtual pet

Saakuru Cashback

Shop online with discount

Saakuru Blockchain

Blockchain with no gas fee

Saakuru Blockchain

Blockchain with no gas fee

Learn more

Saakuru App

All-In-One crypto wallet

Saakuru App

All-In-One crypto wallet

Learn more

More Info

Learn more

Apply for scholarship

TomoOne

Grow virtual pet

TomoOne

Grow virtual pet

Learn more

Learn more

Financial planning and personal budgeting

No matter how healthy your financial situation may be, financial planning and personal budgeting is a great way to manage your money and ensure that you aren’t just meeting your financial obligations, but also maximizing your wealth. Plans and budgets may take a little bit of effort to create at first, but they could save you a lot of stress and trouble in the future.

In this AAG Academy guide, we’ll explain financial planning and personal budgeting, as well as how to make a budget, tackle your debts, and more.

Introduction to financial planning

We all have different goals when it comes to our personal finances. Perhaps you’re looking to buy your first home, start a family, take your dream vacation, or invest some spare cash in hope of a better future. Whether you’re starting small or dreaming big, a financial plan lets you get ahead of your financial commitments and manage your money in the best way possible.

Your personal financial plan doesn’t have to be complex, but there are some key things the best plans take into account. Those are:

Finance tracking

No one wants to spend hours every week updating their financial plan, however, it is important that you occasionally spend a little bit of time updating your figures. You’ll use your plan to track your finances — everything coming in as well as everything going out — so it is critical everything is accurate and that no nasty surprises can pop up when you least expect them.

Financial goals

The most effective financial plans are guided by goals, so it is important to think about what you want to achieve with your money, both in the short term and in the long term. Without setting concrete goals, you have nothing to aim at, which can make managing your money difficult. It’s also easier to waste spare cash if you do not have goals to put that money toward.

Emergency planning

One of your most important financial goals should be to plan for emergencies. In an ideal world, your emergency budget should be around three times your monthly income. This ensures that if you ever find yourself in a sticky situation, perhaps because you’ve lost your job, you have plenty of time to get yourself back on your feet without missing any important bills.

Of course, putting aside three month’s worth of salary payments can be incredibly difficult for many of us, but an emergency budget of some kind is crucial.

Debt management

Another important goal is debt management, particularly when it comes to tackling high-interest debt. If you have credit cards, loans, and finance agreements with high interest rates, it is in your best interest to get these paid off as quickly as possible — before you start putting money aside for other, less important things.

Although it may seem counterintuitive to put more money into your debts when you’re trying to save toward other goals, you will see a big advantage in the long run. Paying off high interest debts faster means you’ll have to pay less interest overall, and the money you’ve saved can go toward other things.

What are the benefits of financial planning?

It is important to note that while a financial plan and a personal budget go hand-in-hand, they are different. While a personal budget will help you manage your finances on a weekly or monthly basis, a financial plan is what you’ll use to set your long-term goals — where you would like to be financially in five, 10, or even 20 years time.

Financial plans are great for those who are hoping to go to college, buy a home, get married, or retire at some point in their future. All these things are significant in terms of their cost, so it is incredibly difficult to achieve them if you do not start planning for them well in advance. That’s exactly why financial planning is essential — and the sooner you do it, the better.

Putting together a financial plan is about more than just jotting down what you hope to attain in the future. It is about putting together a strategy that will help you achieve your goals. If you hope to buy a home, for instance, you’ll need to think about how much it might cost, how much you’ll need for a deposit, and the steps you’ll need to take to get there.

What is personal budgeting?

Regardless of how much or how often you get paid, it is critical that you are mindful of your outgoings in advance and that you don’t leave yourself in a situation where you have important bills to pay, but you’ve already spent all your money. With personal budgeting, you’ll know what expenses are coming up and when — and how much cash you have to play with.

Expenditure planning won’t just improve your financial situation; it will also have tremendous benefits to your mental health if you’re the kind of person who worries about money. When you’re prepared for the week, month, or even year ahead from a financial point of view, there are no surprises, and you’ll save yourself a whole lot of anxiety and stress.

While you can have a personal budget without a financial plan, it is near impossible to have a financial plan without a personal budget. If you aren’t managing your money effectively in the short term, you will not be able to fulfill your goals in the long term. As we mentioned above, most of us have to plan significant expenses, such as buying a home, years in advance.

First step of financial planning

So, let’s get started by creating a personal budget, which is the first step toward financial planning. This may seem daunting at first, but it’s actually pretty simple and shouldn’t take you a great deal of time. These are four key things to consider. These are:

Income

The first thing you’ll want to take note of in your budget is your income. Depending on whether you get paid weekly or monthly, you’ll want to make a record of the total amount you expect to receive, and when you expect to receive it.

Expenses

Once you know how much you have coming in, the next step is to record what has to go out. Some of these expenses — like your rent or mortgage, car payments, loan repayments, and utility bills — will be fixed. They will be roughly the same amount each month, and they will usually be paid on the same day each month. Other expenses will be variable.

Variable expenses include things like groceries, fuel, entertainment, clothing, and transport. It can be more difficult to calculate these things because the cost of them usually varies on a regular basis, so you may choose to work out an average for each one, or, if you want to be really careful, a maximum amount for each one.

One important thing to take into account when calculating your expenses is an emergency fund. If you can afford it, it is an excellent idea to set some cash aside for unforeseen circumstances, such as vehicle or home repairs, or in case your income is unexpectedly reduced in the future. How much you put into this fund is up to you.

Left over

Once you have deducted all your expenses from your income, you’ll know how much money you have left over. What you do with this is up to you. You may choose to save it for a rainy day, invest it into something that could increase your wealth over time, or put more money into debts to pay them off faster. Whatever you do, bear in mind your financial goals for the future.

If your expenses are greater than your income, it can be incredibly worrying, but there may be things you can do to change that. For instance, it may be possible to cut back on your variable expenses, such as entertainment, clothing, and fuel costs. If you eat out or socialize on a regular basis, for instance, cutting back just a little could save you a lot of cash.

Financial checkup

While putting together your personal budget, it is recommended that you perform a financial checkup. This is when you take stock of your overall financial situation and review where your money is going. It’s also a good idea to do this whenever your financial situation changes, perhaps because you got a new job, or got married or divorced.

Part of your financial checkup — in addition to reviewing and potentially setting new financial goals — should be to assess all your debts to find out how much you have left to pay, plus the interest rates for each one. This will help you with the next step of the process, which is debt management.

Debt management plan

Another thing you may want to consider if your expenses exceed your outgoings, particularly if a lot of those expenses are debts, is a debt management plan (DMP). A DMP is an agreement between you and your creditors that takes into account how much you can reasonably afford to pay, rather than how much you originally agreed to pay.

DMPs can be incredibly helpful if your income has been reduced, or you have simply amassed too many debts and are now struggling to keep up with them all. However, there are some important things to consider before you go down this route.

First, a DMP won’t wipe out any of your debts. You will still be liable to pay everything you owe; it may just take longer than originally agreed if you reduce your ongoing payments. Second, creditors will want to know about your personal budget — and specifically how much you can afford to pay — before they will agree to reducing your regular repayments.

Most importantly, you should bear in mind that a DMP may adversely affect your credit rating. While it’s usually not as bad as missing payments entirely, and you may not be able to avoid it if you simply cannot afford your debts, it is worth bearing this in mind if you are relying on a good credit rating in the future, perhaps to get a mortgage.

To set up a DMP, you can either contact your creditors yourself, or enlist a dedicated debt management company that will do this on your behalf for a fee. Depending on where you live, you may be able to get help with a DMP for free from a debt charity.

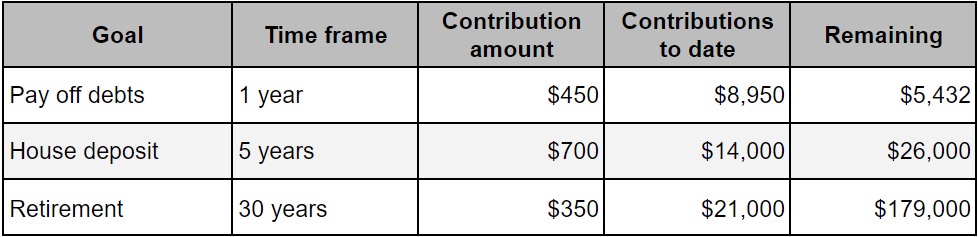

Financial goals, setting financial goals, and examples

Once you have control of your personal budget, it is time to start thinking about your financial goals. Only you can decide what those goals are. For many of us, things like buying a property or setting ourselves up for retirement are common objectives, but everyone is different. Others may want to pay off their debts as quickly as possible.

Setting your financial goals should take into account what you hope to achieve in the short term — perhaps over the next five years — and then what you want to achieve in the long term. Again, only you can prioritize those things and determine what should be achieved first. However, to give you an idea, here’s an example of a basic financial plan:

This example is obviously a very rudimentary one, but it should serve as an example of what a basic financial plan should look like. The more effort you put into your own — and the more time you spend on planning each of your goals — the more likely you are to achieve them.

The example should also help explain why you really need a personal budget before thinking about your financial goals. Without first determining how much money you can spare each week or each month, you cannot calculate how much you want to contribute to your short- and long-term goals, or how long it will take you to achieve them.

Saving without a financial plan, perhaps by simply putting away whatever you can spare each month, may be effective for some people. However, a more concrete plan not only helps you keep track of what you’re working toward, but it can also motivate you to stick to your goals. You may be less inclined to make impulsive decisions with your money if you can see that you’re making real progress toward bigger and better things.

References

- What is a financial plan

- Budget vs financial plan

- Expenditure plan work

- Debt management plans

- Best budgeting software in 2022

Frequently Asked Questions

Financial planning is important because it can help you take control of your money — particularly how much you’re spending — and plan for the future. It is particularly useful for those working toward a financial goal, such as buying a house, or trying to get their finances in order by paying off their debts.

An independent financial advisor can certainly help you out with budgeting and financial planning if you need assistance. However, you’re likely to have to pay for this service. If you need help with debts, you may be able to get free assistance from a charity instead.

That depends on your personal situation and who you go to. You can put together a budget and financial plan yourself, which won’t cost you a penny. If you seek help from a financial advisor or another professional, then it depends on their rate.

If you’re working with a limited budget, simple spreadsheet software like Microsoft Excel or even Google Sheets should be enough to create a budget and financial plan. If you’re looking for something a little more sophisticated, check out FreshBooks, QuickBooks, or Xero.

The process of putting together a budget is the same, regardless of how much you’re earning. However, you will need to think more carefully about how you manage everything if money is tight. Try to keep an eye on variable expenses because you may be able to cut down on certain things to help you save or to ensure that you can stay on top of more important bills.

If you’re struggling to meet debt repayments, consider speaking to your creditors, a financial advisor, or a debt charity about putting together a debt management plan (DMP). This can help ensure your debt repayments are manageable and that you don’t fall behind, which would have an adverse effect on your credit rating.

Was this article helpful?

YesNo

About the author

Disclaimer

This article is intended to provide generalized information designed to educate a broad segment of the public; it does not give personalized investment, legal, or other business and professional advice. Before taking any action, you should always consult with your own financial, legal, tax, investment, or other professional for advice on matters that affect you and/or your business.

Get news first

Be the first to get our newsletter full of company, product updates as well as market news.

🍪

We use cookies to make your experience better. Learn more: Privacy Policy

Accept